Welcome to reThinkable - my weekly newsletter where I share actionable insights to build a wealthy healthy life.

Estimated read time: 4 minutes and 56 seconds

When it comes to building wealth, it's all relative.

While I'm a strong believer in The Box Strategy— where you compare yourself to your past self — sometimes you need to compare yourself to others.

The reason: if everybody's wealth grows by 35%, then you haven't actually gotten "wealthier" because everyone is still in the same relative position.

In order to get ahead, you need to outperform the median.

Today, I'm revealing the median net worth by age for Americans and then sharing 3 techniques high net worth individuals take advantage of.

➡️ Median Net Worth By Age

According to Empower, this is the median net worth by age:

Age by decade | Median net worth |

20s | $7,467 |

30s | $35,435 |

40s | $126,126 |

50s | $290,271 |

60s | $446,703 |

70s | $371,603 |

All in all, the US median household net worth, regardless of age, is close to $192,000.

The reason we're focusing on the median net worth and not the average net worth is because averages are skewed by the super-rich. For instance:

If there are 5 people living in Magic Lamp Town and 3 people have $100 to their names while 2 people have $1,000,000, then the average net worth in that town is $400,060, whereas the median net worth is $100.

Now, your goal is to try to beat the median net worth at every age group.

I started creating financial education content in 2020, and it has grown into something I never imagined. I worked on Wall Street for a few years, got my Economics degree from Vanderbilt, and write nearly everything based on firsthand experience. In just a matter of a few years, I’m now able to help people, just like you, live wealthier and healthier lives.

So If you're looking to achieve financial freedom from someone who has, you've come to the right place. I strongly believe if you surround yourself in personal finance by reading, listening, and watching financial content, you will quickly scale your net worth.

💰 What High Net Worth People Do

The Biggest Contributor

The net worth for the above-median person is heavily boosted from their tax-advantaged investment accounts. Taxes are one of the biggest factors that slow down your personal wealth accumulation, which is why you should take advantage of all the tax-advantaged accounts you can.

For instance, the 401(k) is a tax-advantaged account where you contribute pre-tax dollars, which lowers your taxable income and tax bill. The money then grows without taxes slowing it down.

You can withdraw from your 401(k) penalty-free after age 59.5, at which point you'll need to pay taxes on the withdrawals. However, by then, your marginal income tax rate should be lower since you're retired.

Here are the 5 most common tax-advantaged accounts to look into:

401(k) Plan: Save pre-tax money for retirement; pay taxes when you withdraw.

Roth IRA: Save after-tax money; no taxes on growth or withdrawals.

Health Savings Account (HSA): Save pre-tax money for medical expenses; no taxes on growth or spending.

529 Plan: Save for education; no taxes on growth or withdrawals for school costs.

Traditional IRA: Save money and possibly get a tax break; pay taxes when you retire.

Pick The Right Thing

Other than taxes, the other thing that strangles your net worth is debt. When you're paying hundreds of dollars or more for your credit cards and car loans, it quickly eats up how much you have left over.

But the truth is, you don't want to pay off every debt you have. Instead, you want to focus on high-interest debt — anything with a 7% interest rate or higher.

The problem with high-interest debt is that it always comes with high opportunity costs. Basically, how much you'll lose out on when you choose one option over another.

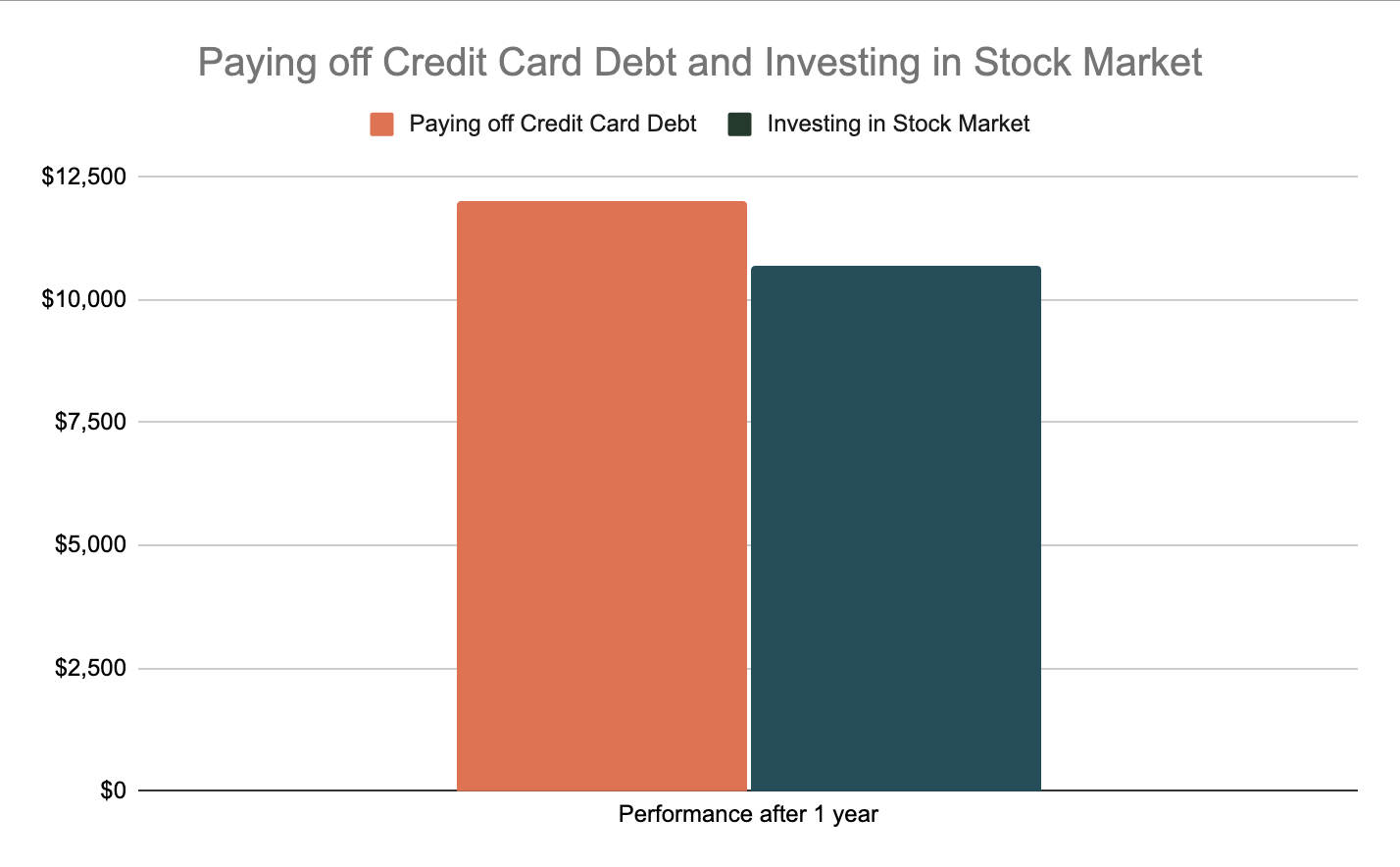

Let's say you have $10,000 cash on hand and you want to do something with it. You have two options:

Option 1: you can completely pay off your $10,000 credit card debt which has a 20% interest rate

Option 2: invest the $10,000 in the stock market, which historically has a 7% average annual return.

If you choose Option 2, in 1 year, your credit card debt will grow to $12,000 since you didn't pay it off. But on the other hand, your investment portfolio would total $10,700 assuming the average return of 7%.

The problem is, with Option 2, you're effectively "earning" $700 from the stock market but losing $2,000 to credit card interest, putting you $1,300 behind compared to if you chose Option 1.

This doesn't mean investing is a bad idea; it's just about priorities and opportunity costs. Paying off high-interest debt is like earning a guaranteed return on investment equal to the debt's interest rate.

By doing this, you're avoiding guaranteed losses from the high-interest debt (>7% interest rate), which is often a much higher "return" than what you could expect from the stock market on average.

Lose Money

No one wants to hear this, but it's true. Making money to outperform the median net worth requires risk.

Even a seemingly "risk-free" trade job like an electrician carries risk. If they come to your house to fix an electrical outage and something catches on fire and burns part of your house down, they run the risk you'll sue them.

Doctors, lawyers, engineers all take risks to work too. Whatever profession you're in right now, you're also taking risks.

Risk-taking is inevitable, so the question isn't “how can you avoid risk,” but rather “how can you maximize the risk-to-reward ratio?”

Alan Watts said, "When no risk is taken there is no freedom."

Many of us actively avoid taking risks. I see it all the time when I’m speaking with aspiring millionaires.

They know what they want but they won't risk a couple bucks to see if they can get it. So they fall short and just wait for something to happen to them, rather than going out there and taking it.

The aim isn't to take a big risk — it's to take a series of small risks.

Invest in yourself, your education, or your ideas. You don't need to quit your job to become an entrepreneur. Instead, balance your work with learning new skills. This will help you earn more money and eventually leave your cubicle job

The main takeaway is just be open to new ideas. Try to be less skeptical and more experimental. This helps you learn what works and what doesn't, bit by bit.

🔎 reThink More

⤴️ Prices might go up soon… thanks to AI

💪🏻 Workers have quit quitting. Here’s what they’re doing now.

💵 The price of this has increased 3x faster than inflation and no one seems to care

❤️ Community Space

In last week’s newsletter, I asked “Why is it important to normalize talking about money?” 91.18% of you got the right answer.

The answer: Because it helps break down taboos, leading to better financial literacy and healthier money habits.

📝 reThinkable Quiz

P.S. here’s a pointy thing enjoying a snack.

If you enjoyed today’s newsletter, share it with your friends and family!

Was this forwarded to you? Sign up here.